Brady Narayan, 22, and Emily Peak, 21, are looking to buy their first home and see benfit in the Coaltiion’s Super Home Buyer Scheme. Picture: Aaron Francis

For hopeful Melbourne buyers Brady Narayan and Emily Peak, being able to borrow money from their super would see them finally leave the family nest and get their first home.

The apprentice electrician, 22, and receptionist, 21, have been squirrelling away money for the better part of three years. They are now at a crossroads – they can either continue to save for another 18 months or get a loan from their parents.

“We obviously don’t have massive wages coming, but we are slowly trying to save to get a deposit to buy a first home together,” Mr Narayan said.

“We could buy something at the moment but we would have to get a loan from our parents. I’d rather use my super and do it myself than put a burden on our parents.

“When there is good opportunity there, I want to buy it when I see it.”

Buying a home will give them freedom and not just because they will they both be able to move out of their parents’ homes in the Liberal-held seat of La Trobe, in outer-eastern Melbourne.

The young couple’s combined savings stand at $30,000 and they are looking for a home between $500,000 and $600,000 in the capital city’s outer eastern suburbs.

The Australian spoke to the couple leaving an open home at a two-bedroom bungalow in Ferntree Gully, in Liberal frontbencher Alan Tudge’s electorate of Aston, as they sought to get a feel for the market and what they hope to buy in the future.

It was a coincidence that Mr Narayan checked his superannuation balance last week, which is around $15,000.

Under the Morrison government scheme announced on Sunday, he would be able to withdraw up to 40 per cent of the balance to purchase a home, which would need to be returned with a portion of capital gains upon sale.

“I think getting into the property market is pretty important,” Mr Narayan said.

“I’m not thinking about retirement yet or what is in my super, that number doesn’t really matter to me.”

It was too late to change Mr Narayan’s vote, however, as he has already cast his because he will be working on election day.

“I was an early voter anyway so it’s too late,” he said.

Melbourne-based mortgage broker David Thurmond, principal of Mortgage Choice Berwick, is helping the couple get their finance.

He believes the scheme will be beneficial given the deposit is the biggest hurdle for most.

“The facts are if a buyer is only missing savings, I don’t see this as diving into the market too soon,” Mr Thurmond said.

“If they can service the debt, they are good to go.”

Mackenzie Scott is a property and general news reporter based in Brisbane. Prior to joining The Australian in 2018, she was the editorial coordinator at NewsMediaWorks, covering media and publishing, and editor at travel and lifestyle website Xplore Sydney.

Copycat Labor not matching Morrison’s housing scheme shows how industry super funds dictate their policy

by Judith Sloan The Australian 17 May 2022

Prime Minister Scott Morrison and first homeowners Andy and Caitlin at their new digs in Wangaratta, Victoria. Picture: AAP

I’m not sure leaving the best to last is good politics, but the Coalition’s Super Home Buyer Scheme is good policy. By allowing potential first home buyers to access a portion of their own savings – mandated through superannuation contributions – to bridge the deposit gap, it should enable more young folk to get into the housing market.

The idea is relatively straightforward: individuals/couples will be able to withdraw up to 40 per cent of their superannuation balances, up to a cap, to be used to purchase a first home.

Variants of this policy apply in a number of countries, including Canada, New Zealand and Singapore.

When the house is sold, the withdrawn amount plus a proportion of any capital gain is deposited back into superannuation, to be used for the purpose of providing income in retirement.

Morrison’s idea is straightforward: individuals/couples will be able to withdraw up to 40 per cent of their superannuation balances, up to a cap, to be used to purchase a first home. Picture: NCA NewsWire/ David Crosling

The fact that Labor hasn’t me-too’ed this proposal is actually good news because it reveals the extent to which the self-interested industry super funds dictate Labor policy. Any policy that allows the withdrawal of funds, even temporary, will always be opposed by these funds.

The argument that superannuation is for retirement and not housing is contradicted by the fact that the majority of retired persons, both now and in the future, relies on the Age Pension, in full or in part. Superannuation may be a helpful add-on for a comfortable retirement, but it is not the be-all-and-end-all.

And here’s the most important aspect of this debate: the strongest correlate of poverty in old age is not owning a home. That’s right – for older folk who continue to rent, particularly in the private sector, the outcomes are grim compared with those who own their own homes.

What this means is that the primary object of policy should be to enable as many people as possible to own their homes, an objective above ensuring adequate retirement incomes, particularly given the Age Pension. (They might even use their final superannuation balances to pay off the mortgage.)

On current trends of home ownership, it is likely that a lower proportion of older people will be homeowners in the coming decades unless there is a significant turnaround in ownership rates.

The Prime Minister visits the Singh family at their new home in the outer suburb of Donnybrook, in WA. Picture : NCA NewsWire / Ian Currie

As to the argument that the Coalition’s policy will simply drive home prices up, the truth of the matter is that all demand-side measures run this risk – and this includes a number of Labor’s own housing policies, including its ill-thought out shared equity scheme.

In the case of the Super Home Buyer Scheme, there is no reason to think there will be a flood of withdrawals as long as the policy stays in place. Individuals/couples will make their own decisions about the timing of accessing their superannuation to buy their first homes, which in turn will depend on their personal circumstances and the state of the housing market at that time.

CONTRIBUTING ECONOMICS EDITOR: Judith Sloan is an economist and company director. She holds degrees from the University of Melbourne and the London School of Economics. Original article here

Federal election 2022: Supply-demand balance ‘as safe as houses’

By Geoff Chambers, The Australian 17 May 2022

Scott Morrison says his housing scheme will ensure Australians are ‘better off’ in retirement. Picture: Jason Edwards

Scott Morrison’s super homebuyers scheme aims to fast-track first house purchases by about three years and ease long-term pressure on the age pension, with the Coalition promising to avoid a price bump by balancing supply and demand.

The Prime Minister said the scheme, allowing first-home buyers to access up to $50,000 or 40 per cent of their nest eggs, would ensure Australians are “better off” in retirement.

Contrasting the Coalition’s no-strings-attached super housing policy with Labor’s plan to claim a 40 per cent stake in the first homes of low-and middle-income earners, Mr Morrison said “we are reinforcing people’s retirement savings” and addressing supply issues by providing incentives for empty-nesters to downsize.

Anthony Albanese joined union super funds and Paul Keating in lashing the government’s election eve policy, slamming it as “not a good idea” and an “attack on future savings … on future generations”.

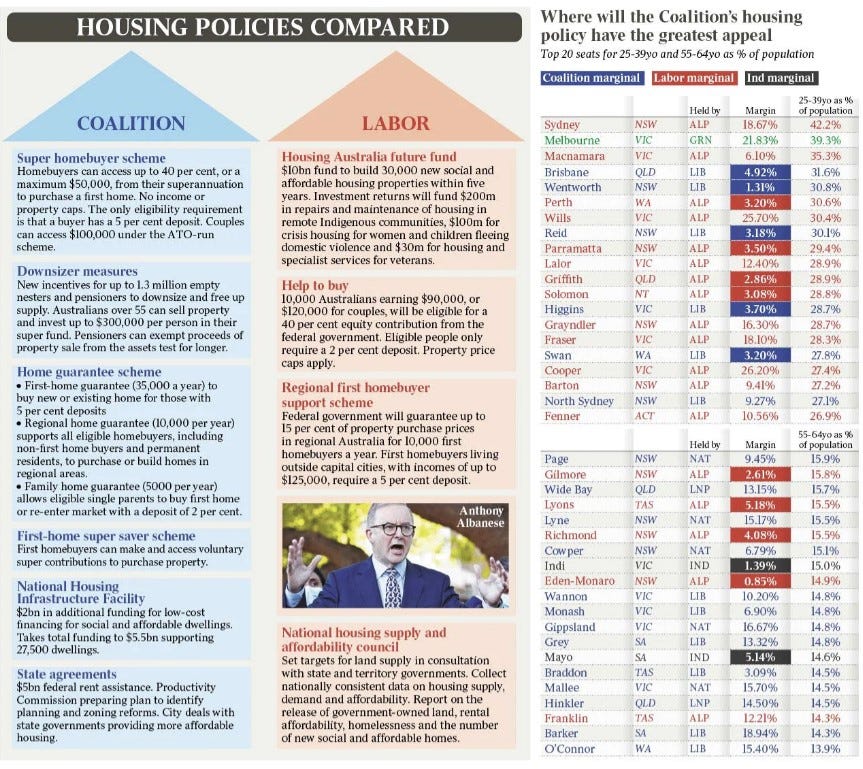

Analysis of census data by The Australian reveals nine of the top 16 electorates with voters aged 25-39 are marginal Coalition and Labor seats, including Brisbane, Wentworth, Reid, Parramatta, Solomon, Higgins and Swan.

North Sydney, which is under threat from Climate 200 and Labor, and Mr Albanese’s electorate of Grayndler also feature in the top 20 seats with the highest percentage of potential first-home buyers.

The top 20 seats with voters aged 55-64, who are being targeted by the Coalition with incentives to downsize, include the battleground electorates of Page, Gilmore, Lyons, Eden-Monaro and Braddon.

Ahead of ramping up his campaign schedule in coming days across battleground states, Mr Morrison visited the Labor-held Queensland seat of Blair and must-hold Cairns-based electorate of Leichhardt on Monday to sell his housing policies.

“The number one issue that forces up housing prices in this country is insufficient supply. And this (super) policy, the downsizing policy, the HomeBuilder policy has all been about increasing and supporting that supply, and that’s what can put down the pressure,” Mr Morrison said.

“I know Labor doesn’t like this idea. I know Labor doesn’t want you to have access to your super.

“I know they think that those who run superannuation are more important to them than you are to them because they won’t let you get access to your money.

“They want to keep your money in someone else’s control. I don’t agree with that. I just don’t agree with it. It’s your money and it should be your home.”

The competing housing affordability policies from Coalition and Labor, which have become a centrepiece of the election campaign, are contrasted by longer-term pledges and stricter conditions on ALP pledges.

While Labor has matched most of the government’s housing policy offerings, it will not support using superannuation to help buyers into the market.

Speaking in the marginal Liberal-held Perth seat of Swan on Monday, which Labor is confident of winning, Mr Albanese said the government had released a “thought bubble” with no modelling.

“They have no idea what the impact will be. If you take super away from people, then you’ll have higher deficits and bills from the government in the future,” Mr Albanese said.

“What super is about is making sure that people can retire with a decent income. If you gut people’s super savings, that means down the track more people dependent upon the pension, more pressure on budgets in the future.”

The 2020 retirement income review, led by former Treasury deputy secretary Mike Callaghan, said owning a “home is the most important component of voluntary savings and an important factor influencing retirement outcomes”.

“Homeowners have lower housing costs and an asset that can be drawn on in retirement. If the decline in home ownership among younger people is sustained into retirement, there will be an increasing number of retirees who rent,” the review said.

“The system favours homeowners, such as through the exemption of the principal residence from the age pension assets test.

“Most household wealth for people aged 65 and over is held outside the superannuation system, with owner-occupied housing the largest asset for most retirees.”

The super homebuyer scheme, which the government says will have an “immaterial impact on the superannuation system”, is estimated to reduce the time taken to save for a deposit by about three years.

Government analysis of the scheme says even if all of the average 100,000 first-home buyers per year bought a median-priced property, the “combined value of their home purchases would be less than 1 per cent of the current value of the housing market, which is valued at $9.9 trillion”.

“On average, there are around 100,000 first-home buyers each year. Even if all of them were to access their super, it would still add less than 1 per cent to property transactions given that there was $687bn in housing turnover in Australia in 2021,” the government analysis said.

With $3.5 trillion in superannuation assets under management, the government says if every first-home buyer accesses the full $50,000 from their super every year, “it would amount to $5bn being withdrawn from the super system”. “This equates to 0.14 per cent of total superannuation assets and around 3.6 per cent of annual contributions.”

CHIEF POLITICAL CORRESPONDENT: Geoff Chambers is The Australian’s Chief Political Correspondent. He was previously The Australian’s Canberra Bureau Chief and Queensland Bureau Chief.

PM’s super property pitch makes more of a difference in cheaper cities

By Michael Read, Australian Financial Review 17 May 2022

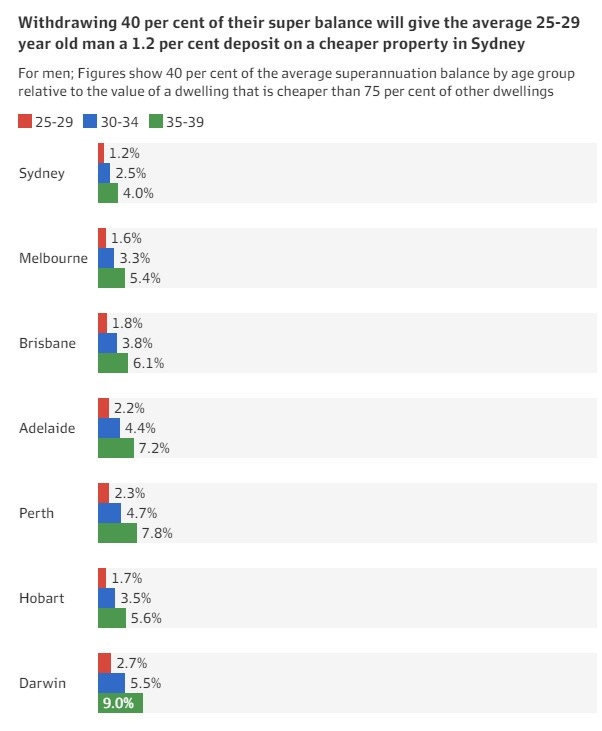

The Coalition’s super for housing proposal will make only a modest dent in the time taken to save for a deposit for young, single Australians in the country’s most expensive capital cities.

The combination of elevated property prices and low superannuation balances means the government’s proposal to let people withdraw 40 per cent of their super, up to a limit of $50,000, will give prospective home buyers only a small boost to their deposits.

But couples, especially those looking beyond Sydney and Melbourne, will derive a larger benefit.

To withdraw $50,000, a person would need to have superannuation savings of $125,000, a sum the average Australian does not accrue until they are in their 40s.

The average 30-34-year-old male has $51,175 in super, meaning they can withdraw $20,470 under the Coalition’s policy. The average female in this age bracket would only be able to pull $16,896 out of their $42,240 super balance, according to data from the Association of Super Funds of Australia. The average couple in their early-30s would have access to $37,366.

Superannuation balance estimates are from 2019, so they predate the impressive sharemarket returns experienced over the past two years, which would have pushed retirement savings higher. The S&P500 is 37 per cent higher than in mid-2019, while the S&P/ASX200 is 12 per cent higher.

They also do not incorporate the effect of the government’s early access scheme, where 3 million Australians collectively withdrew $36.4 billion from their retirement savings during the pandemic. Individuals were able to withdraw up to $20,000 across two tranches.

Because of low superannuation balances, the gap between what people can withdraw from their super under the Coalition’s policy and the deposit required to buy a property in a major capital city is large for those under 35.

The average man in his late-30s who used the scheme would unlock a 4 per cent deposit on a cheaper property in Sydney and 5.4 per cent on one in Melbourne. The average woman in this age group would acquire a 3.2 per cent deposit on a place in Sydney and 4.3 per cent in Melbourne. A cheaper property is one that costs less than 75 per cent of other properties.

The policy will provide a bigger boost to couples. The average couple in their late-30s would have access to a 7.2 per cent deposit on a cheaper property in Sydney and 9.7 per cent in Melbourne.

It will provide a bigger boost in cheaper housing markets such as Perth and Adelaide.

This is before any potential increase in property prices, with Superannuation Minister Jane Hume saying on Monday she expects a “bump” in property prices as a result of the measure.

Withdrawing 40 per cent of super will give the average 25-29-year-old man a 1.2 per cent deposit on a cheaper property in Sydney.

The average woman in that age group would have a 1 per cent deposit on a cheaper property in Sydney, a 1.4 per cent deposit on a similar property in Melbourne, and 1.6 per cent on a modest place in Brisbane.

The controversial pitch to let people tap their super comes as the downturn in Sydney’s property market gathers pace, with prices falling for the third month in a row in April to a median value of $1.1 million.

Speaking to The Australian Financial Review, Senator Hume said the government decided to limit withdrawals to 40 per cent of a person’s balance because it did not want Australians to “empty their super” to buy a house.

“We want to make sure that people continue to contribute to superannuation and continue to build their retirement savings.

“But at the same time, we’d want to unlock [super] so they can buy a house now and even further ensure their economic security and retirement by owning their own home.”

Senator Hume did not say how large the “bump” in house prices would be.

“Inevitably, if you put out a demand-side measure as the Coalition has done, and as the Labor Party has done, there will be a small and temporary effect on demand.”

Senator Hume said any decision to release the modelling underpinning the policy was “a decision for after the election”, but said the policy had been “carefully calibrated”.

She said measures to encourage older Australians to downsize and deals to unlock land supplies would keep a lid on prices.

Michael Read is a reporter based in Parliament House, Canberra. He was previously an economist at the Reserve Bank of Australia and at UBS. Connect with Michael on Twitter. Email Michael at michael.read@afr.com.au

Super bosses must embrace Coalition’s super plan: Robert Gottliebsen

By Robert Gottliebsen The Australian 18 May 2022

Superannuation bosses must understand the importance of the Coalition super plan to the long term future of the industry. Picture: Damian Shaw/NCA NewsWire

It is really sad for the superannuation movement in Australia that the current crop of fund executives don’t understand the importance of the Coalition superannuation measure to the long term future of superannuation.

Forget the politics. An increasing proportion of younger Australians not only see superannuation as irrelevant to their lives but as a source of advantage to older Australians that they do not deserve.

That view, which has validity, is likely to gather greater momentum in the years ahead and will almost certainly result in eventual dismantling many of the superannuation advantages that currently exist and a long term reduction in its importance. .

In a world where people are worried about the impact of climate change, saving for retirement seems an irrelevancy but higher rents are underlining to the younger generation, and even to those coming up through the education system, that there are real advantages in owning your own dwelling.

The absurdity of having money stuck in superannuation and not being able to access it for housing creates a deep frustration with the older generation’s rules that is clearly not understood by those running our superannuation funds.

As the Retirement Incomes report clearly set out ownership of a dwelling is the best pillar for a person entering retirement. Superannuation comes second.

Like me, our superannuation fund managers come from a previous home owning generation who could take advantage of superannuation.

The fund executives have not realised that, over time, superannuation frustrated young people in the community will swamp the media and eventually destroy superannuation as we know it.

We must recognise their situation is different to previous generations and they have to be brought into the equalising tent.

Offering access to superannuation to help buy a house is a vital first step. My criticism of the current proposal is that it is not generous enough and that greater access should have been announced perhaps including limited access to future contributions for those that have demonstrated a clear savings pattern.

The wonderful aspect about the plan is that the vast majority of first home buyers will eventually sell their first dwelling and the money returns to mainstream superannuation. One of the criticisms of the Morrison plan is that it will boost house prices. In normal times that would be a valid criticism.

Indeed, some years ago, along with others, I could see the looming issue and I was writing strongly in favour of allowing young people access to their superannuation to buy a dwelling.

But I stopped once the housing market took off because in that environment such a stimulation would have sent house prices up even further. But now the game has changed. Holders of some 30 per cent of the housing loan stock will be damaged by a rate increase above 1.5 per cent. And. as I will explain below, there is a now a greater prospect of such an event.

By far the biggest force causing movement in house prices is the availability of bank credit. Whereas bank money was almost limitless six months ago, now it is now much more restricted. It is a perfect time to enable first home buyers to access their superannuation without pushing up house prices.

In recent days, I have spent some time moving around a number of industries. I am beginning to challenge the Commonwealth Bank’s belief that a 1.5 per cent interest rate rise will be sufficient to curb rising inflation. A large number of employers actually want worthwhile wage rises because they hope it will attract more people into the work force.

Those importing from China are seeing 10 to 15 per cent price rises beginning to come through. Add to that oil and food. But demand is holding.

Just as significant, the vast number of enterprises that have been maintaining their profits by holding back on maintenance and capital improvements are now at last beginning to rectify the problem. Engineering enterprises conducting maintenance are seeing a big rise in demand and linked to that demand are clear signs that companies are updating their equipment and investing in technology.

We have the chance to move into a society with a higher rate of inflation than we are used to but one which will not stagnate despite higher interest rates. .

One of the vulnerable groups in that environment are those that over borrowed at low interest rates who must fund large rises in their bank loan repayments.

Higher wages will help but they won’t off set much bigger payments that will be required if the interest rate rise is above 1.5 per cent.

The impact will certainly moderate our economy and when combined with the bank housing credit squeeze it will put considerable pressure on house prices – a perfect time to allow first home buyers to access their superannuation.

BUSINESS COLUMNIST : Robert Gottliebsen has spent more than 50 years writing and commentating about business and investment in Australia